Market overviews

•

Shop Talk: Agentic Commerce

Agentic Commerce is one of AI’s most ambitious bets. Since 2025, the promise has been bold: AI agents would hunt deals, negotiate prices, manage subscriptions, and execute purchases autonomously while we sipped coffee.

Both a16z and Sequoia have rallied behind the thesis, painting a trillion-dollar future for whoever builds the “next Amazon.” McKinsey mapped a $3–5 trillion global opportunity by 2030 (with $1T in US B2C alone), while Grand View Research projected agent-initiated transaction value to clear ~$8 billion in 2026. But consumer behavior told a more honest story.

While Gen AI traffic to retail sites surged over ~4,000%, actual agentic conversion remained negligible. OpenAI pulled back from Instant Checkout in March, pivoting to dedicated in-ChatGPT apps after merchants reported the original didn't drive sales. Perplexity's ‘Buy with Pro’ was supposed to make agents the new checkout, but has since gone dark.

Clearly, the hype leapfrogged the technology. Most “agentic” implementations were simply advanced chatbots or rules-based automations, exposing the lagging commercial readiness and critical gaps like messy product data, non-agent-friendly APIs, fragile payment rails, and trust issues.

Instead of consumer-facing agents, eager incumbents (Shopify, Amazon, VISA, Stripe) and ambitious startups (Profound, t54 Labs, Runlayer) are now doubling down on the foundations first, such as protocols, data standards, and payment infrastructure.

The Agentic Commerce Ecosystem: A war of protocols

Agentic commerce requires a common language—a standardized way for AI agents to discover products, negotiate, and transact with merchants and payment systems, similar to how HTTP standardized the web.

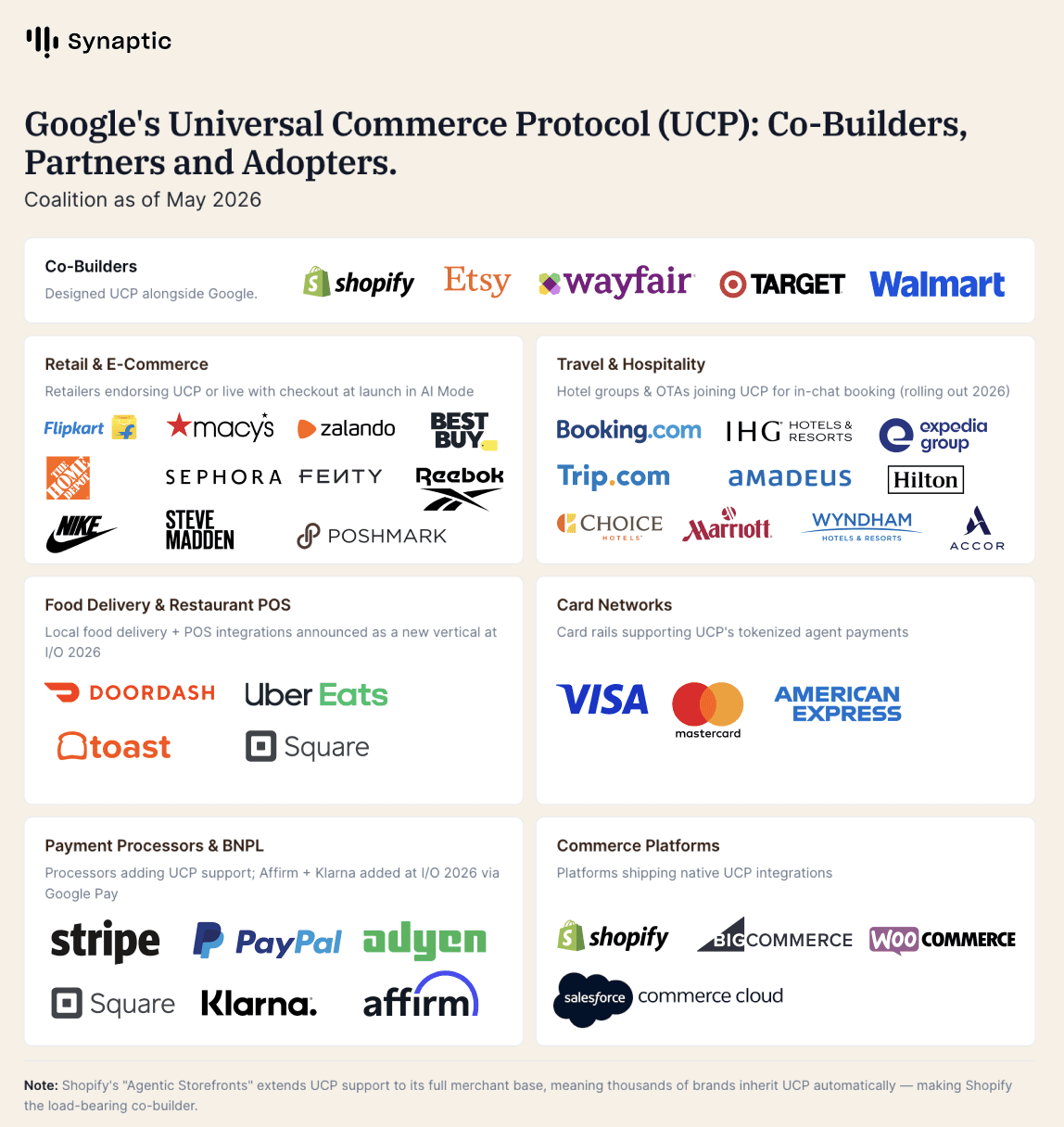

A four-way race to define the standard is on, and already leaning in Google’s favor with the release of Universal Commerce Protocol (UCP).

Protocol | Primary Backers | Focus Area | Key Reach |

|---|---|---|---|

ACP (Agentic Commerce Protocol) | OpenAI + Stripe | Instant checkout & single-item purchases | ChatGPT, Microsoft Copilot, 1M+ Shopify merchants |

UCP (Universal Commerce Protocol) | Google + Shopify, Walmart, Target, Etsy | Full shopping journey (discovery to post-purchase) | Broad retail coalition (20+ endorsers including Visa, Mastercard) |

MCP (Model Context Protocol) | Anthropic (donated to Linux Foundation) | Secure context sharing & tool integration | Open standard, high SDK usage |

AP2 / A2A (Agent 2 Agent) | Google + payment networks | Agent payments & agent-to-agent interoperability | Mastercard, PayPal, etc. |

Google co-developed UCP with Shopify and is endorsed by 20+ partners, including Visa, Mastercard, Stripe, American Express, Walmart, Target, Home Depot, etc. It is open-source and built on three existing primitives: Agent Payments Protocol (AP2), Agent2Agent (A2A), and Model Context Protocol (MCP).

Google has taken an early lead with UCP, recently supercharged at Google Marketing Live 2026 with the launch of Universal Cart, expanded support for Food & Travel, and new merchant tools. However, OpenAI + Stripe’s ACP remains strong in checkout execution, while Anthropic’s MCP is becoming the de facto standard for secure agent capabilities.

No major merchant wants to bet on a single protocol to avoid platform lock-in. Most are multi-homing aggressively as they integrate with both UCP and ACP simultaneously. Visa (Trusted Agent Protocol or TAP) and Mastercard (Agent Pay) have stayed neutral in the protocol war — supporting multiple protocols while maintaining flexibility across authentication and authorization flows. This positions them to win regardless of which protocol ultimately dominates.

Google’s UCP also has strong adoption among traditional big-box and established retailers (Wayfair, Best Buy, Home Depot, Macy’s, BigCommerce), while OpenAI + Stripe have gained traction with conversational commerce players (Instacart, DoorDash) and several fashion/lifestyle brands.

Beyond interoperability and standards, the market is still grappling with the dynamics of customer ownership: If agents become the primary interface for commerce, who controls discovery, trust, and purchasing behavior? Every partnership signed in 2026 is a positional bet on that answer.

If agent runtimes become the new browser, OpenAI and Anthropic control discovery and charge merchants for placement. If they become the new search box, merchants stay in control, and runtimes get commoditized.

Google is hedging both sides. OpenAI/Stripe is doubling down on transaction execution. Anthropic is focusing on open, secure foundations.

Interestingly, open-source is also pushing back. The Linux Foundation and LF AI & Data are developing neutral open standards to counter proprietary capture by Big Tech and frontier labs.

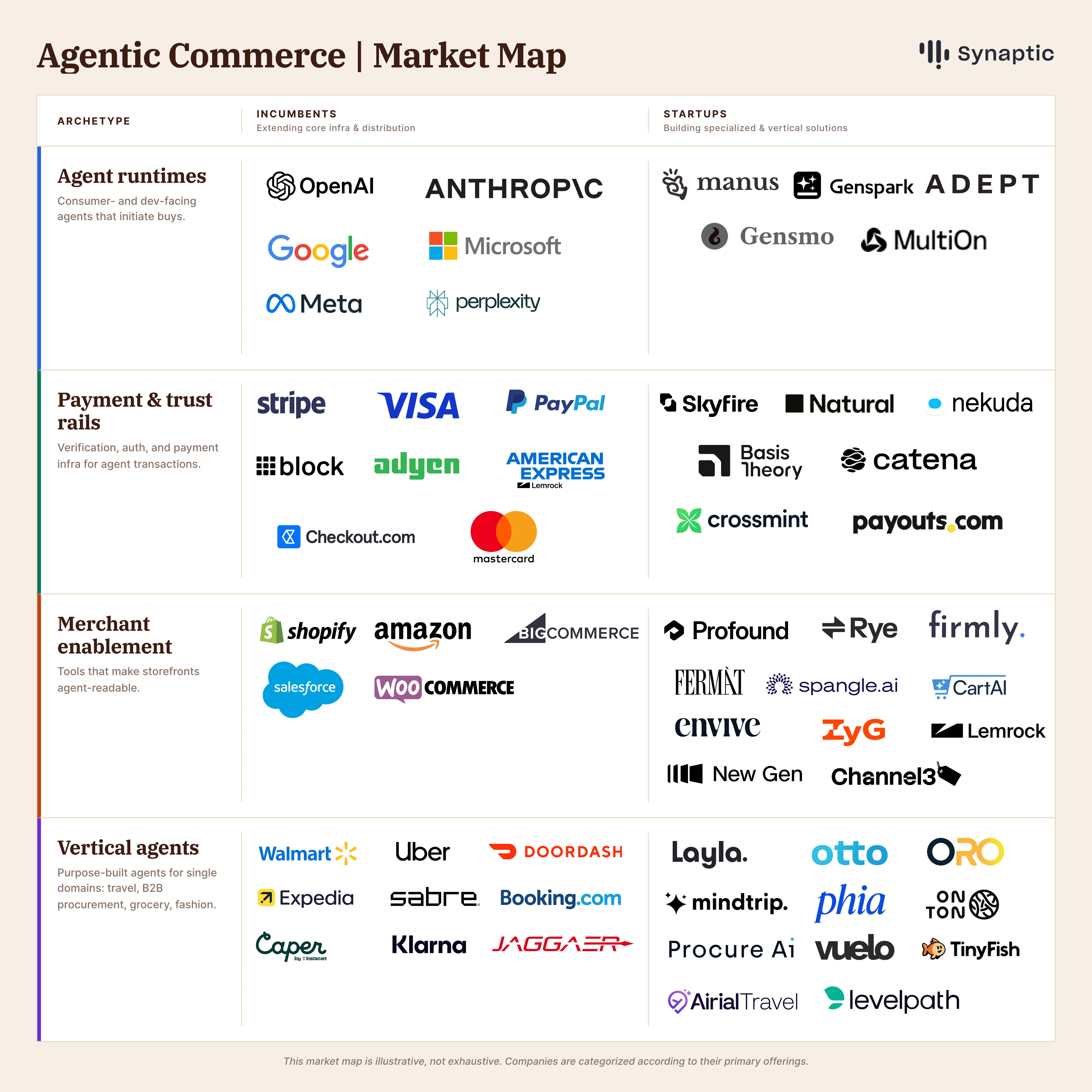

Player Archetypes: Startups are racing to be the agent, while incumbents are racing to own its rails

The agentic commerce stack has settled into five layers, each with its own startup-vs-incumbent dynamic.

Agent runtimes: Operator, Perplexity, Claude, Manus, and Genspark are the primary consumer-facing agents that initiate purchases. This is the layer where users directly interact with agents.

Payment & trust rails: Building the verification, authentication, and payment layer for agent transactions. Stripe, Visa, Mastercard, and PayPal are creating their own protocols (Agentic Commerce Protocol, Trusted Agent Protocol, Agent Pay), while startups like Skyfire, Nekuda, Payman, and Catena Labs are building the foundational primitives these protocols will eventually need. Incumbents will likely acquire these startups rather than rebuild what they have already solved. Expect tuck-in M&A through 2026.

Vertical agents: Agents built for one type of purchase: a flight, a grocery basket, a procurement

contract, a fashion drop, or an ad placement. They control the full process: product catalog, workflow, and often the checkout itself. While serving a narrower market, they deliver higher conversion rates and stronger, SaaS-like customer retention.

Some early winners include Mindtrip (Travel), Auger (B2B procurement), Instacart's agent stack (grocery), Daydream (fashion), and a growing crop of media-buying agents in advertising.Trust, identity & fraud: Agent KYC, transaction verification, and merchant-side fraud layer helping merchants distinguish "good bot" from "bad bot.” They can verify agent identity, confirm when transactions are genuinely intended, and give merchants a way to allow legitimate agents while blocking fraudulent ones.

Legacy fraud stacks were built for humans and cannot catch what is new here: prompt injection, agent identity spoofing, and synthetic shopping bot rings. Agent-native challengers like Verisoul, Lakera, and Trustible are building directly for these threats.Merchant-side enablement: Making storefronts agent-readable by turning product catalogs, inventory, and checkout flows into usable data for agents. Shopify's agent endpoints, agent-optimized product feeds, and MCP servers can expose catalog and inventory data directly to agent runtimes.

This is also the foundation on which everything else depends—when product data is unstructured, agents cannot browse, compare, or buy effectively—yet startup funding remains surprisingly thin.

Market Map: Trust, Checkout, and Identity are becoming the new battlegrounds

The agentic commerce market is in its early but explosive growth phase, with incumbents and startups sharing a largely symbiotic relationship. Startups are building the new payment and checkout layers, while larger incumbents are partnering with or buying them to expand merchant reach and improve trust and security features.

Most startups are filling the gaps where incumbents move slower: agent-native identity and payments (Skyfire, Basis Theory, Nekuda), universal checkout across fragmenting merchants (Rye, Firmly), and merchant enablement/optimization tools.

Merchant enablement remains incumbent-heavy via platform extensions (Shopify, BigCommerce), leaving startups strongest in shared infrastructure that can plug into many platforms and become hard to replace.

Keycard, t54 Labs, Runlayer, and Oasis Security have built trust and identity infra for non-human agents — a category that didn't even exist 12 months ago.

Vertical agents are clustering in two places: travel (Vuelo, Mindtrip, Layla, Otto, Airial) and B2B procurement (Oro Labs, Procure AI, Levelpath).

Startup activity in ‘Checkout’ remains thin despite its importance—most agents still fail at final execution due to fraud blocks and fragmentation.

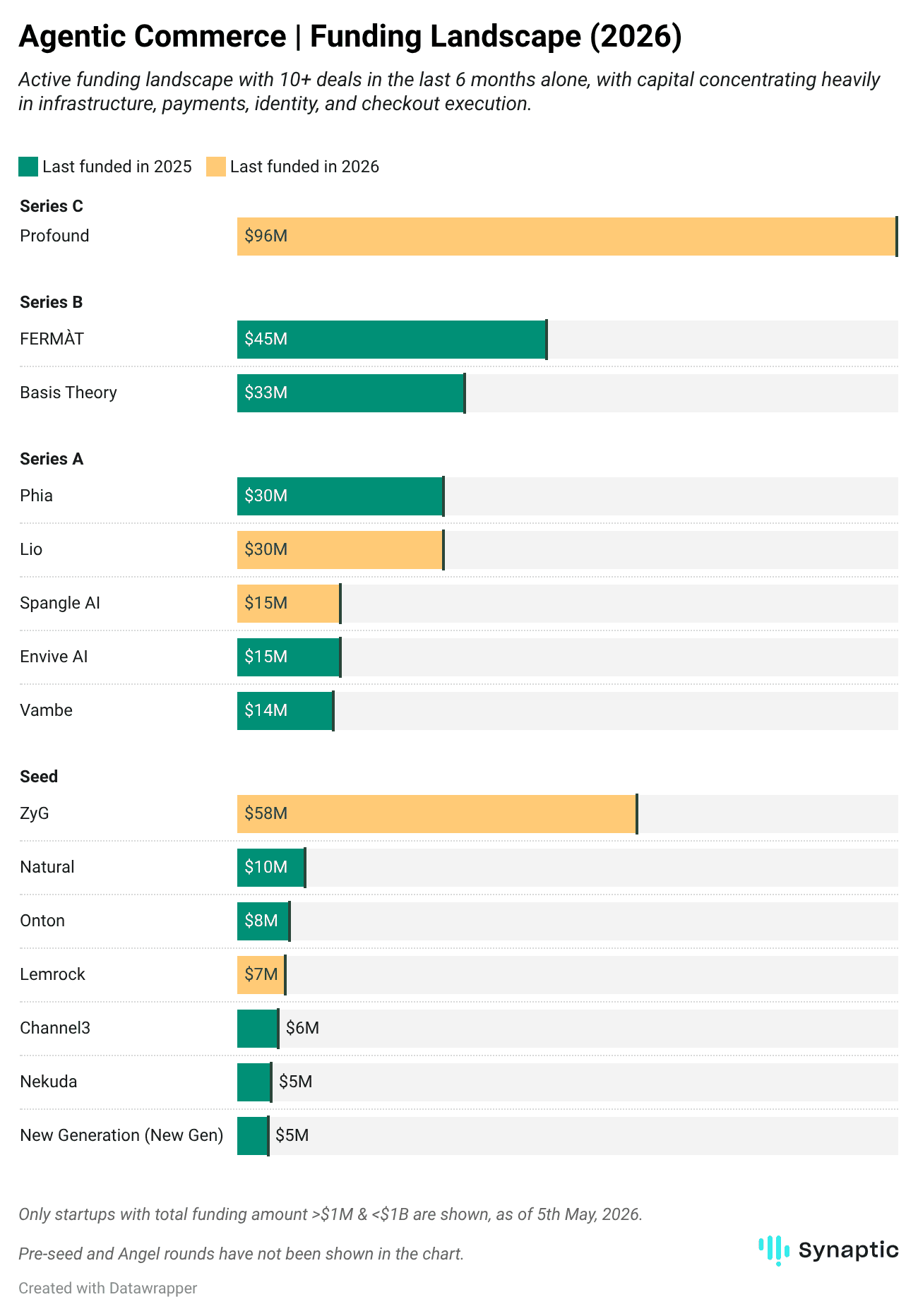

Funding Landscape: VCs are making infrastructure-first bets, as incumbents continue the M&A spree

Startup funding has concentrated heavily in the payments, identity, and infrastructure layers.

Capital is flowing across three main tracks: dedicated rounds for agent-to-merchant infrastructure startups, strategic M&A by incumbents acquiring agent-native tools, and multi-billion-dollar mega-rounds for general-purpose agent runtimes, where commerce is just one of the many ways to monetize.

Payments and identity segment has attracted the majority of disclosed early-stage capital. Stripe, Visa, Mastercard, Google, and PayPal are actively investing in or partnering with startups while developing their own protocols and tools, providing strong market validation.

Distribution is becoming more important than funding size, and the market is starting to reflect that. Founders with strong industry relationships and distribution may have a bigger advantage than founders with the largest funding rounds. Nekuda raised just $5M but became a Visa launch partner. Basis Theory raised $33M and brought together the Agentic Commerce Consortium, an industry coalition uniting AI innovators, researchers, and payment networks.

Merchant enablement is producing breakout names. FERMÀT is building an AI-native commerce platform designed for both human and AI-agent shoppers. Spangle AI helps storefronts adapt dynamically to shopper context, while Envive AI builds self-improving AI agents focused on conversion, retention, and visibility across generative search.

At the seed stage, Lemrock (€6M, March 2026), Channel3 ($6M, December 2025), and New Generation ($4.5M, 2025) raised rounds for catalog middleware powering ChatGPT, Claude, and Perplexity (10M+ live products), a 50M+ universal product database, and AI-native storefronts with embedded Visa payments, respectively.

The M&A market is also consolidating the rails layer faster than any other part of the stack. Stripe's $1.1B acquisition of Bridge, closed in February 2025, brought stablecoin rails inside ACP within 12 months of ACP's launch. PayPal acquired Cymbio in February 2026 to power Store Sync, feeding merchant catalogs into Microsoft Copilot and Perplexity. And in March 2026, Mastercard announced its $1.8 billion acquisition of stablecoin firm BVNK after Coinbase's earlier $2 billion bid collapsed in November.

The China dimension is starting to matter more and more. Meta's blocked acquisition of Singapore-based Manus by China's NDRC in April 2026 was the first agentic-commerce-adjacent deal to hit jurisdictional limits.

Expect more bifurcation between US-aligned (OpenAI, Anthropic, ACP/AP2) and China-aligned (Alibaba, ByteDance, Manus) stacks as the market evolves.

Key Challenges

Protocol fragmentation is breaking interoperability faster than the standards bodies can fix it. Merchants supporting only one protocol are not automatically reachable by agents using another. Most large retailers are forced to implement both ACP (OpenAI + Stripe) and UCP (Google + partners) simultaneously. This multi-protocol burden increases integration costs and results in partial coverage for many agent runtimes.

Regulation is moving faster than most of the category expects. The FTC is actively examining AI transparency and disclosure requirements, while the EU AI Act imposes obligations on high-risk autonomous systems. State UDAP laws already apply to misleading agent behavior. Many current agent flows would struggle under strict enforcement of disclosure, consent, and accountability rules.

Liability, chargebacks, and hallucination have no clear industry playbook yet. When an agent buys the wrong thing, the wrong color, at the wrong price, or hallucinates a SKU that doesn't exist, who eats the cost? Card networks, merchants, and issuers have not agreed on responsibility for agent errors, leaving merchants exposed in most cases.

Permissioning and transparency are the consumer-facing trust problem nobody has solved. Most current systems rely on broad, one-time consents (“buy anything under $X”). This approach risks eroding trust when things go wrong. Building granular, contextual, and easily revocable consent mechanisms that give users clear control is the unsolved challenge.

These foundational challenges explain why infrastructure and trust layers are attracting the bulk of investment today. Until they’re solved, agentic commerce remains more vision than reality.