Market overviews

•

Unsupervised Learning: AI Edtech Tools

Generative AI is poised to transform how educational content is developed, personalized, and consumed.

For instructors, AI can generate lesson plans, course content, assignments / quizzes, and tailored instruction to meet a wide array of learner needs. Gradescope AI is helping teachers grade a class of 250+ in 15 minutes. Edapp’s AI-Create saves 81% instructors ~2 hours of time while creating course content.

For learners, AI are capable of generating interactive and adaptive coursework that can challenge them at their individual pace and skill levels. Personalised AI tutors like Flint can provide instant feedback and support, filling in gaps in understanding – a feature that has led to clear increase in engagement at certain K12 institutions.

Gen AI can also empower self-learners with curated learning content based on prompts, summarized research papers for quicker understanding, and translated educational material to unlock global content.

Gen AI in Edtech can democratize learning on an unprecedented scale. However, it poses a significant challenge to upholding academic integrity – a struggle that is compelling institutions and instructors to reimagine assignments. Read on for an overview of the space.

AI in Edtech: Powerful use cases for Instructors and Learners, but also potential for misuse

Gen AI can take learning beyond the one-size-fits-all approach

Gen AI can curate learning content that dynamically adjust to each student's unique pace, learning style, and proficiency level. As a chatbot, it can also act as a 24x7 tutor which a learner can mould as per their needs and their pace.

Empathetic LLMs can be a gamechanger in education. As empathy scores of LLMs improve over time with training and fine-tuning, Gen AI can act as a teacher with limitless patience and the ability to give focused attention to every single learner, thus eliminating the time- & resource-limitations of traditional educational methods.

AI's capacity to create unique and immersive content paves the way for a new kind of interactivity in educational materials. Imagine history lessons where AI brings historical figures to life through interactive dialogues (e.g. Character AI) or science classes where complex concepts are illustrated via AI-generated simulations.

AI can craft lesson plans tailored to curriculum standards and student data, generate quizzes that target areas needing reinforcement, and provide instant feedback on answers, revolutionizing the backend of education. This automation lifts a considerable burden off instructors, allowing them to dedicate more time to the human-centric aspects of teaching such as mentorship and emotional support.

Misuse of AI in academic content needs regulation and better AI-content detectors

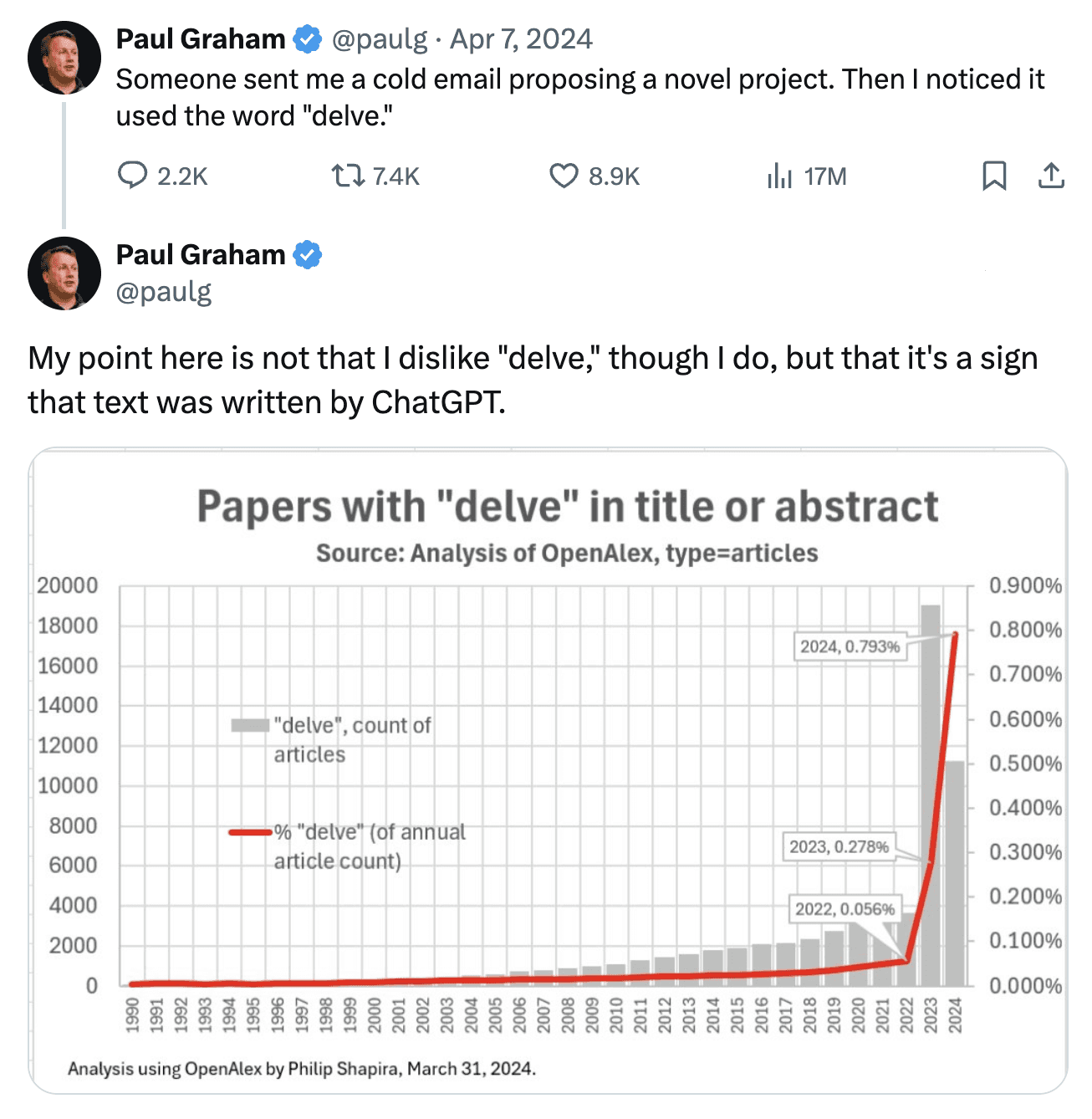

89% of K12 learners were using ChatGPT to write their homework in 2023. It’s a similar story in higher-ed and academic researchers. The pervasiveness of AI-written content has raised several concerns amongst instructors, and brought forward the need for error-free AI-detection tools.

Limitations of current AI-detection tools have been pointed out by several researchers. At the same time, instructors in higher-ed are wary of AI detectors incorrectly flagging human-written content as AI-written. Institutions like Cornell have introduced guidelines and frameworks to help instructors encourage ethical use of AI in their courses.

The increasing usage of the “delveˮ in academic papers – a word often overused by ChatGPT suggest a possible rise in AI-generated content in research.

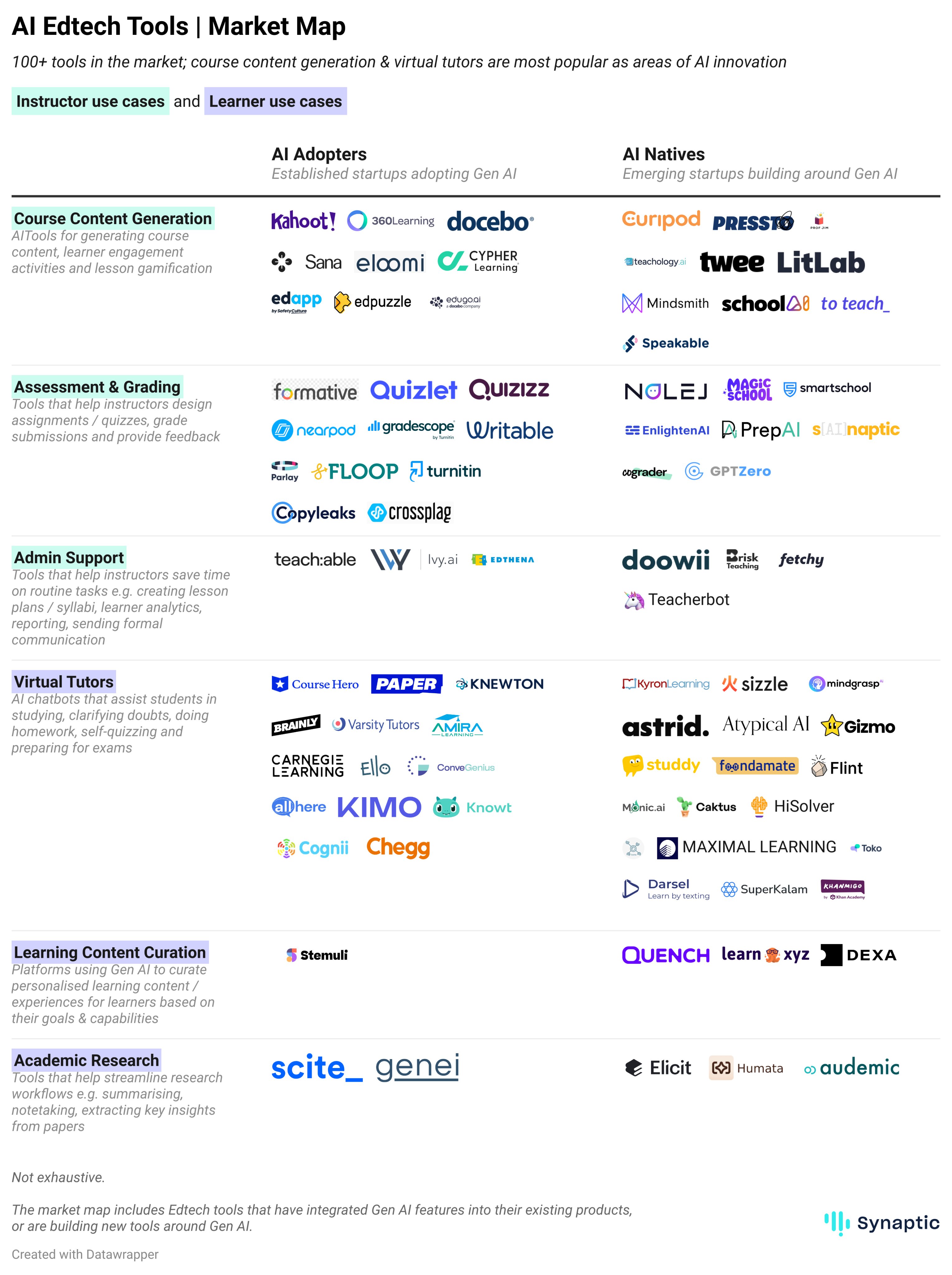

Market Map: Thriving market with 100+ AI-native & AI-adopter tools innovating with Gen AI

Large market with diverse use cases, opportunity for multiple startups to play & innovate

Similar to the AI Video Tools market, the AI Edtech market has a diverse set of prosumers (i.e. users who create content for others to consume using these tools) and consumers with several use cases – making it an attractive playground for startups to innovate.

These prosumers include teachers across K12 to Higher-ed, L&D instructors, and casual creators in learning communities (e.g. Skillshare) who are looking to create quality course content, automative routine tasks like writing lesson plans & grade reports, and engage learners with interactive assessments.

Consumers, i.e. learners of all ages & attributes who have specific needs such as getting help with homework / revision / exam prep, learning to write better, and upskilling provide a large lower-end market. Both of these target segments present a solid opportunity for new startups to build niche solutions.

Chatbot-based Virtual tutoring is a focal area for emerging startups

Virtual tutor tools make up for ~40% of the AI-native tools present in the Edtech market. Virtual tutors deliver personalised learning material to learners at an optimal pace, continuously analyze their responses and performance to provide realtime adaptive feedback and identify areas of strength and weakness.

Startups are building for downstream use-cases like AI homework assistance (Sizzle AI), spoken language learning (Toko), and mentoring for specific exams (SuperKalam).

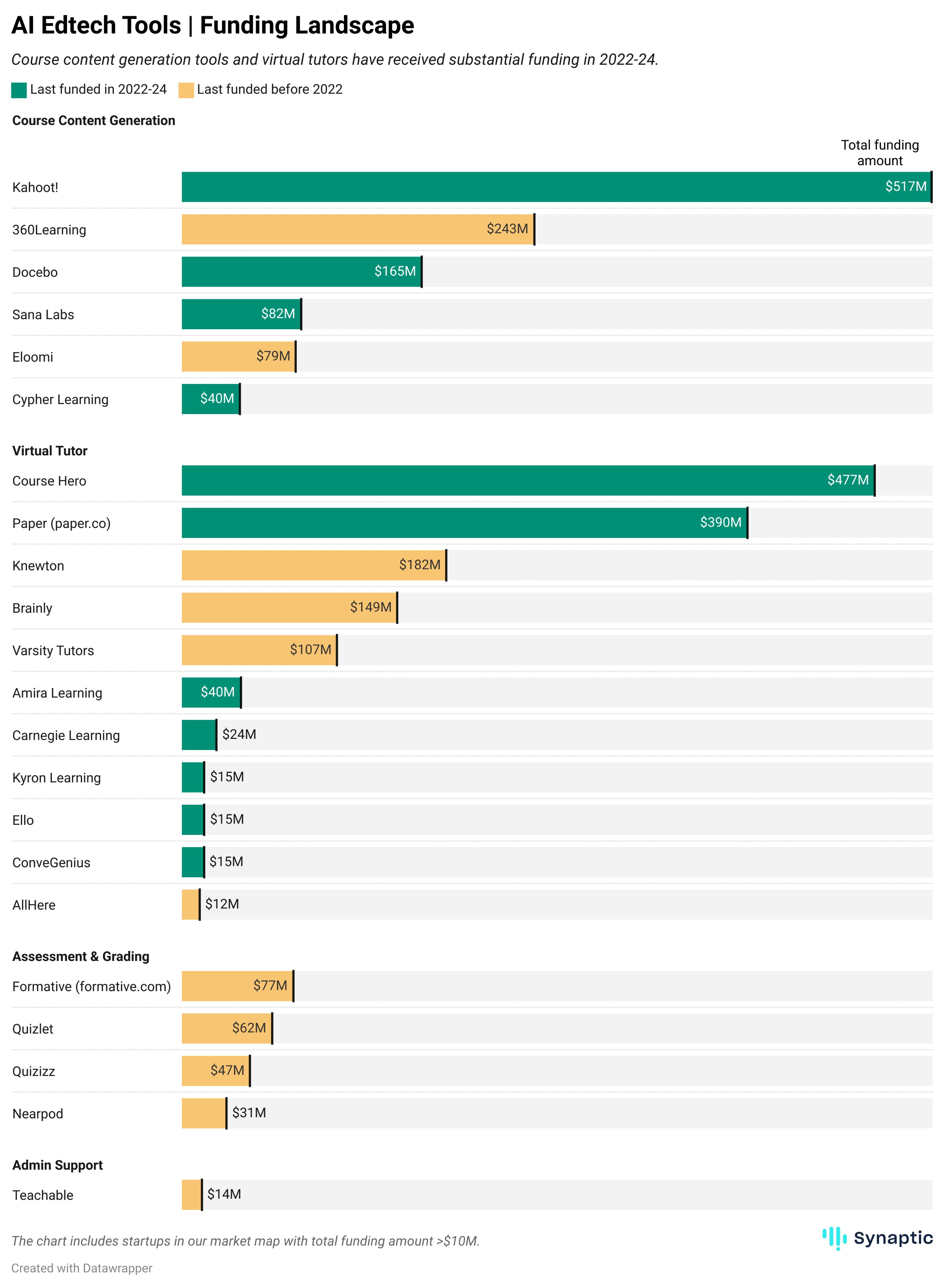

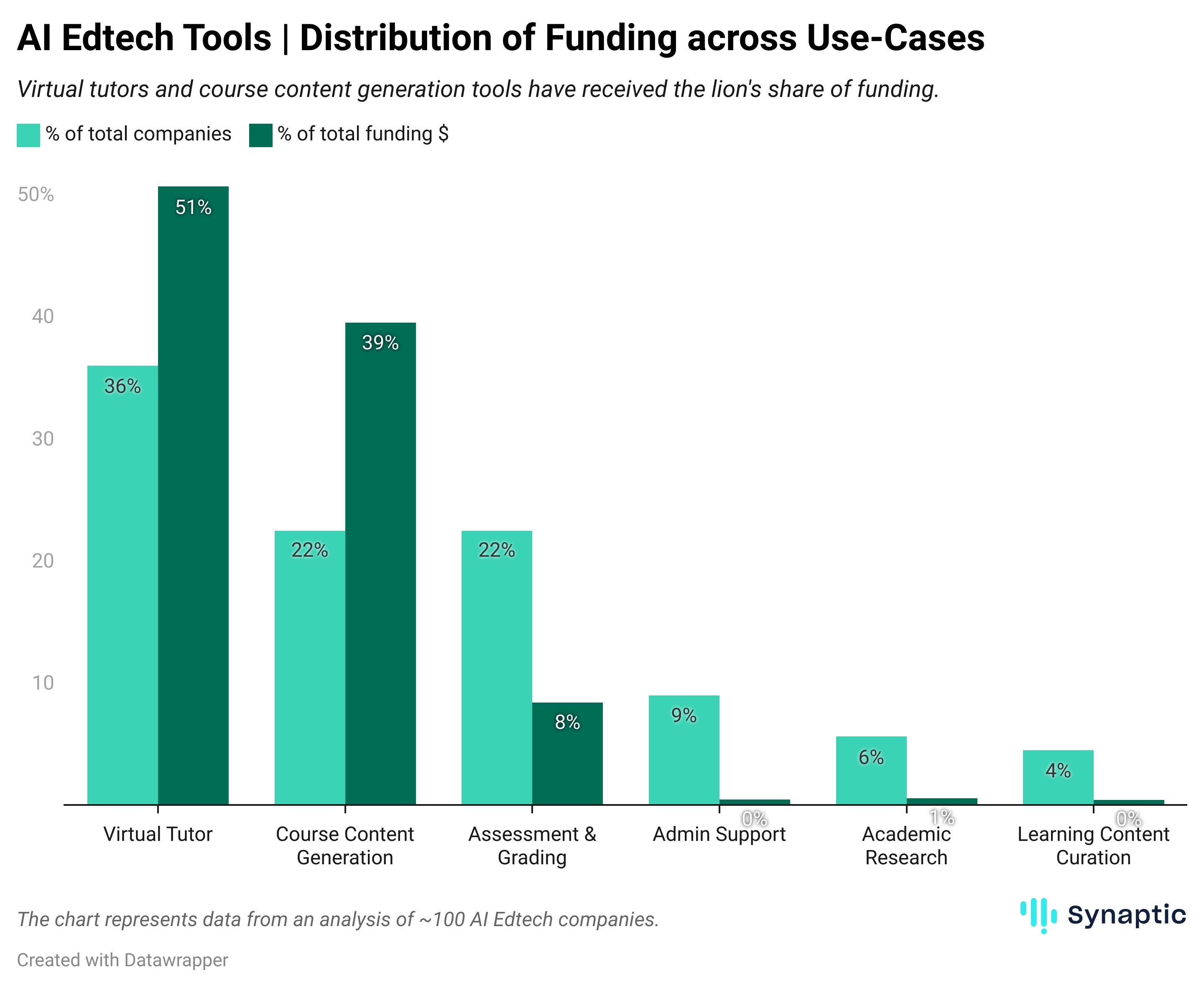

Funding Landscape: Virtual Tutor tools have garnered the maximum share of funding

AI-native tools have received limited funding, only 6% of the total funding dollars

There are 2.5x more AI-native tools than AI-adopter tools in the market, yet their combined funding in 2022–24 has been only 7% of the funding that AI-adopters received. AI adopters, i.e. established players with proven scalability have attracted the majority of funding.

GSV Ventures, Reach Capital, and Owl VC have been prominent investors in the space, participating in 5–8 deals each.

AI-native startups likely need to show clear differentiation to attract VC funding. Many of the current AI-native startups in Edtech have built an API to foundational models like GPT, and added UI/UX wrappers around it – which isn’t a strong differentiator.

Finetuning these models with unique, use-case specific datasets will be key to gaining a competitive edge – something that established startups like Gradescope (with student essays) and Kahoot (with quiz questions) have done.

Virtual tutors and course content generating tools have received the most amount of funding

Virtual tutors and course content generators make up about 60% of the market, but have received almost 90% of the funding in the space. A key reason behind virtual tutors having above 50% of the investment dollars is that the segment includes a number of well-established, 100M+ funded companies like Coursehero, Paper, Brainly.

Significant M&A activity in the space, 10+ deals since 2020

Goldman Sachs’ acquisition of Kahoot!, Research Solutions’ acquisition of Scite and Docebo’s acquisition of Edugo.ai are some recent examples of M&A activity in the space.

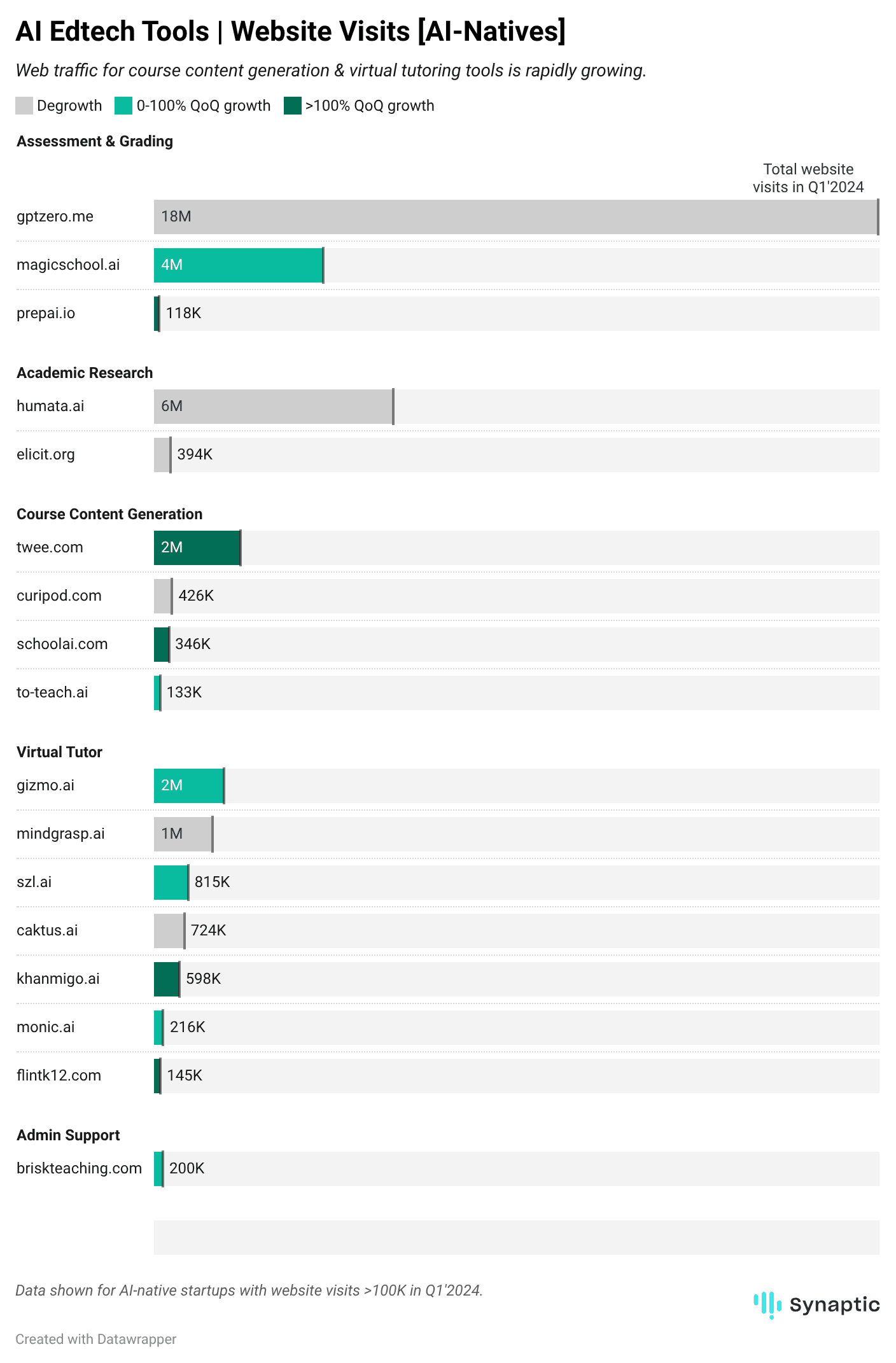

Website Visits: Surging interest in course content generators & virtual tutors; Magicschool AI, Twee, Gizmo are gaining traction

Magicschool offers 60+ AI tools / templates for instructors for specific use cases such as generating syllabus, parent-teacher communication emails, lesson plans, report cards and more, reportedly saving instructors 10+ hours a week. They’re the latest winner of the Global ASU+GSV Summit Cup.

Twee is an AI tool for English Language teachers that facilitates generation of questions, dialogues, stories, and more from text excerpts or YouTube videos. Twee comes with several built-in AI prompts and lesson plans for instructors to kickoff their journey with.

Gizmo is an AI app that personalizes the learning process for students. It enables learners to generate their own flashcards and quizzes, utilize spaced repetition and active recall to boost memory retention, and engage in peer-group learning.

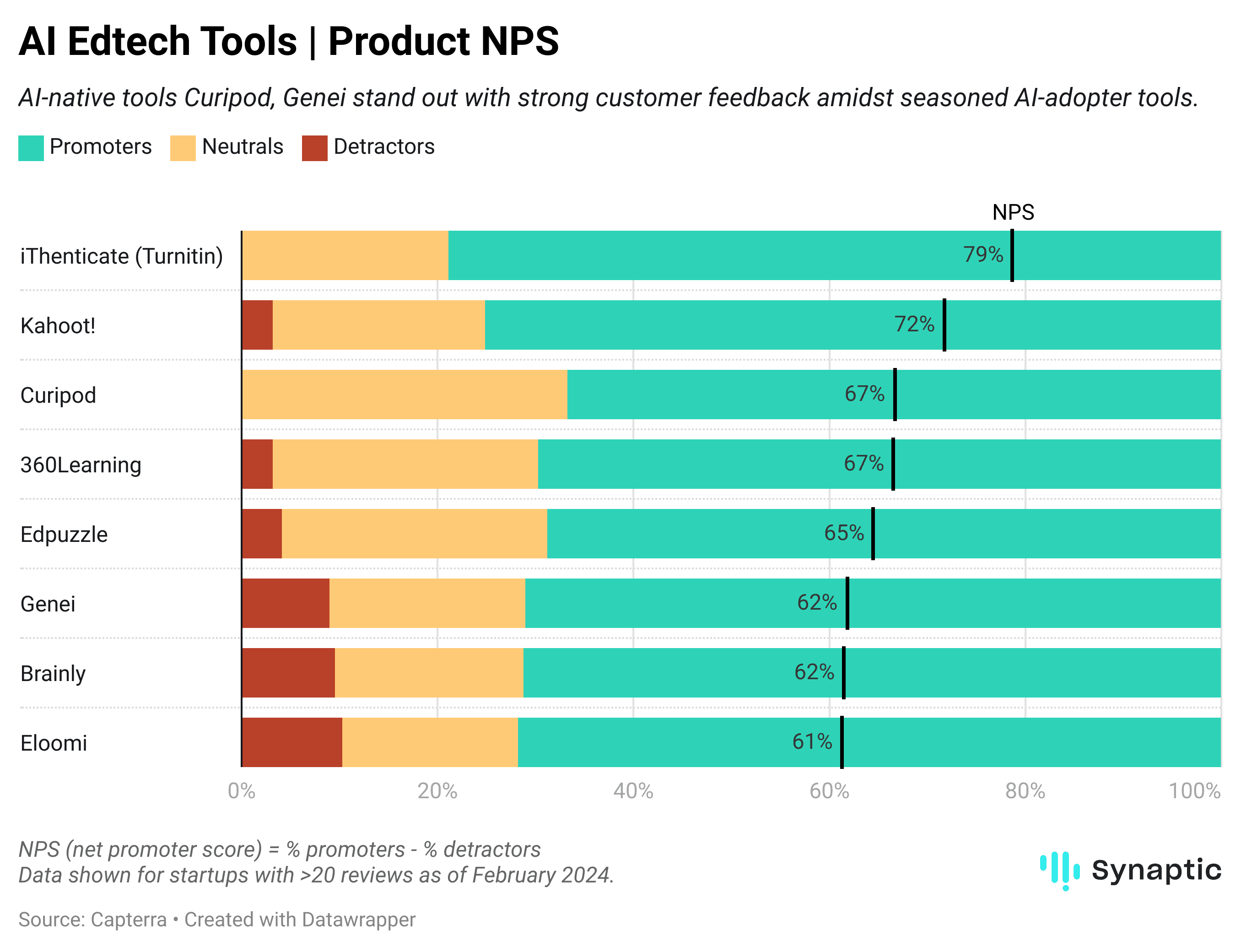

Product Reviews: AI-native tools Curipod, Genei have received positive customer feedback

While established AI Adopter tools like iThenticate, Kahoot! are leading in product NPS, 2 AI-native tools have made their mark with respect to customer feedback:

Curipod uses Gen AI to enable teachers to generate interactive lessons on any topic and give students individual feedback on written responses.

Genei is an AI research assistant that streamlines multiple workflows for researchers and academic writers, such as extracting key information from a library of papers / articles, planning a structure for writing, and generating citations.

Looking Foward

Personalised learning is the frontrunner for AI usecases in Edtech, especially for new entrants

Personalised learning is the most exciting use case of Gen AI in Edtech. Platforms like Magicschool, Curipod, School AI, Kyron Learning, Monic.ai are helping both instructors and learners from K12 to workplaces personalise study material and learning activities viz. quizzes, flashcards as per their own requirements. Future startups in this space will likely offer more nuanced solutions – AI virtual learning environments / simulations is an untapped area that could see future innovation.

Well-funded established startups that have adopted AI will cater to enterprise use cases

Enterprise software in educational institutions / workplaces are often entrenched. Established tools like Kahoot!, Coursehero, Gradescope already have a foothold in such institutions and will likely continue to build further AI features or acquire new tools with niche use cases, e.g. Amira Learning (reading coach), CoGrader (grading assistant).

Expect an active M&A landscape

10+ mergers have occurred in the AI Edtech market since 2020, such as Goldman Sachs’ acquisition of Kahoot!, Research Solutions’ acquisition of Scite and Docebo’s acquisition of Edugo.ai. More M&A activity can be expected within EdTech in the coming years as bigger players acquire the capabilities to expand their market share.