Market overviews

•

Raising the Bar: AI Legal Tools

The application of large language models (LLMs) to the Legal profession is a niche but promising use case. A recent report by Goldman Sachs claimed that ~50% of all current tasks in the legal profession could be replaced by AI - indicating a huge opportunity. Allen & Overy's recently announced partnership with Harvey (an AI legal chatbot), that makes the chatbot available to all their ~3,500 lawyers, underscores this opportunity. And where there is opportunity there is startup activity - from new AI-native offerings to established Legal Tech players adding AI to their core offerings, the Legal Tech space is evolving fast. Here is an introduction to the market and what to watch out for in 2023.

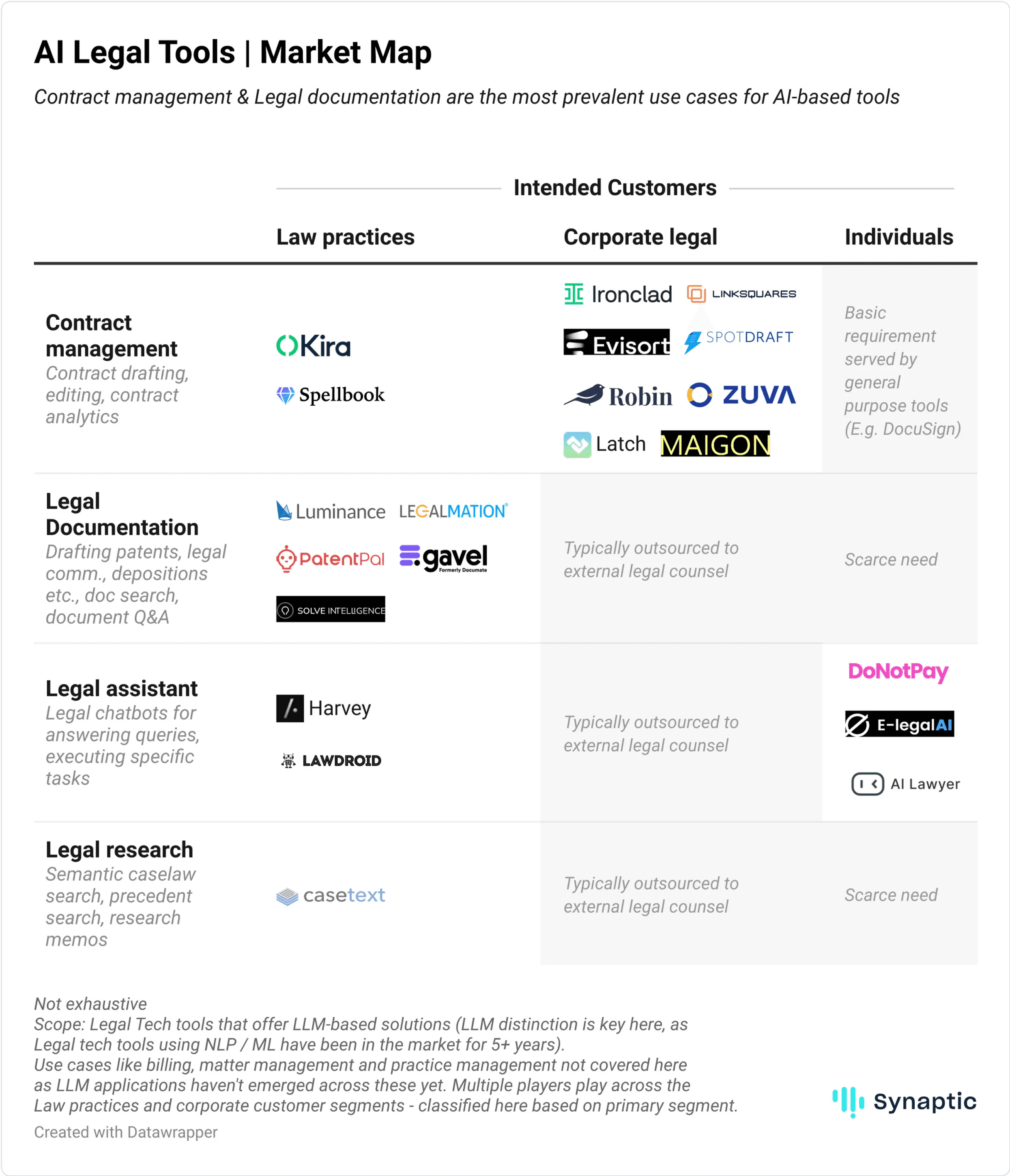

Market: Nascent space with startup activity focused on Contract Management and Documentation use cases

Two points of context on Legal Tech are important to know before delving into AI Legal Tools:

It’s a Solar system - Large incumbents like Thomson Reuters, Lexis Nexis and Aderant are staples in the law firm middle/back office tech stack. Legal Tech ecosystem has evolved around these tools, focusing on specific value-adding use cases.

Not all AI is equal - AI tools built with NLP / ML at their core have been common in the space since as early as 2015, you would be challenged to find a startup in the space that doesn’t have “AI” in its description. For this analysis, we’ve focused on tools that are utilizing LLMs, which we believe are a major step up from NLP / ML and will unlock transformational value for legal use cases.

Contract management has been a growth area for Legal Tech over the last 5 years driven by a large TAM (as every company deals with contracts, and contract automation adds significant value) and the fact that you can sell products to corporates, thus avoiding a run-in with the large incumbents at law practices. Contract management tools offer contract drafting / editing, execution and contract analysis features. The application of LLMs has largely been on contact drafting - stepping up template-based drafts to auto-generated drafts from a prompt. Ironclad, LinkSquares and Evisort are series C+ startups with established customer bases that have invested in LLM-based functionality.

Legal Documentation tools serve primarily 2 purposes - a) finding information across a large set of documents, also called e-discovery (for e.g. finding relevant facts in a data dump submitted by a counter-party during litigation) and b) drafting documents like patent applications, legal communication etc. (some tools also provide contract drafting features in conjunction). LLM application has largely been on drafting as of now.

Legal assistants are an LLM-native concept that has emerged primarily over the last year. The concept is similar to ChatGPT and GitHub Copilot in creating a chat-based interface for a broad range of assistance. The number of tools exploring this use case are low currently, primarily because of the high accuracy requirement in legal advice. Harvey however has taken a novel approach to crack this market (more on it to follow). DoNotPay has created a new market for automated B2C legal advice, focusing on small disputes that lawyers wouldn't pick and customers would typically drop (e.g. rebates, parking tickets etc.). Tools like E-legal AI and AI Lawyer are also exploring legal chatbots for individual customers for simplifying legal jargon, asking basic legal questions etc., however the use is very nascent.

Legal research has been dominated by Westlaw (Thomson Reuters) and Lexis Nexis - every law practice more or less has access to these tools. Research thus hasn’t been a focus area for startups. Casetext is an exception - it was an early adopter of GPT-3 in 2020 to provide powerful semantic search and has been able to scale off of that.

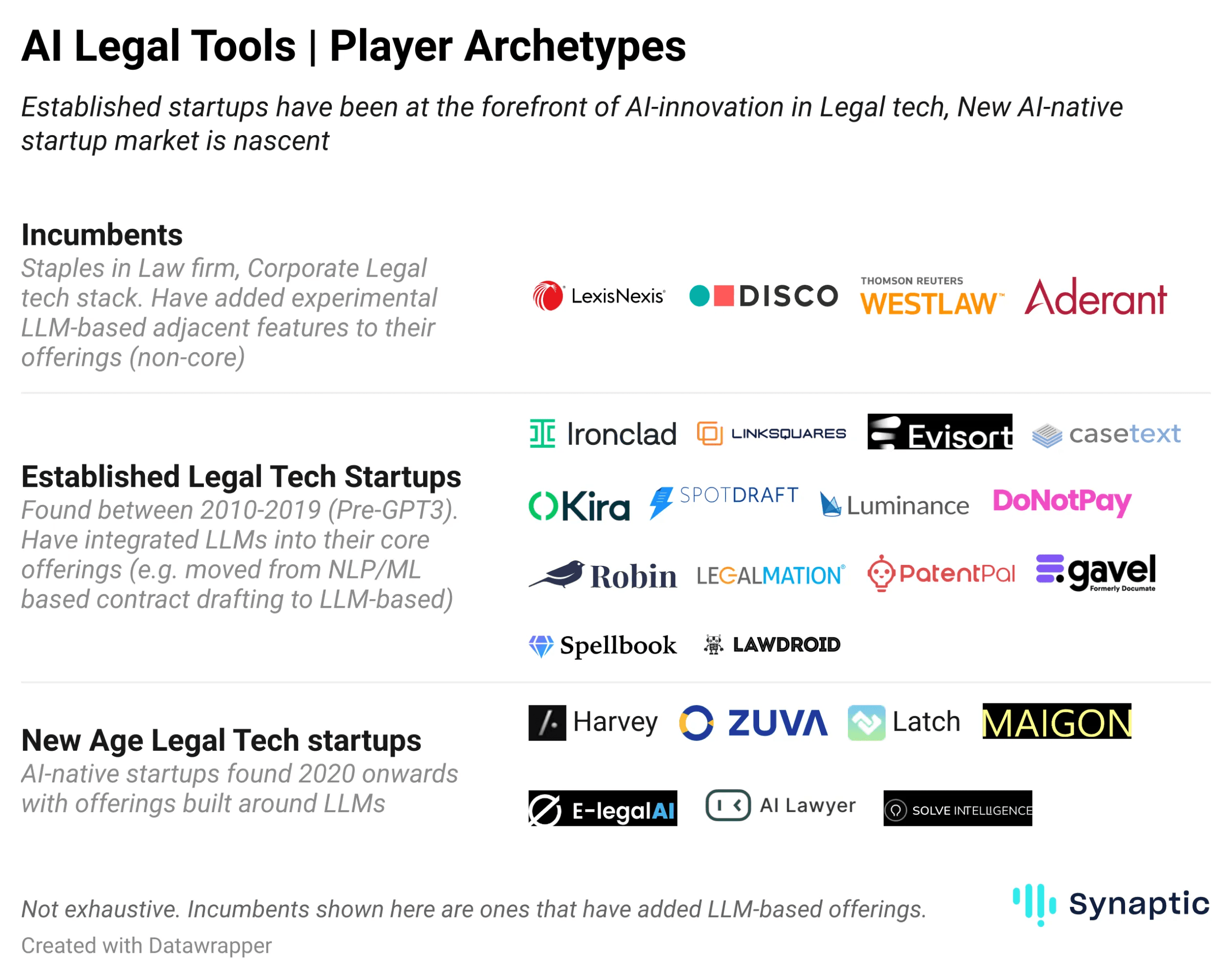

Player archetypes: LLM applications have been pioneered by Established Legal Tech Startups, AI-Native Startups are nascent

In markets like Copywriting and Coding tools, a large set of AI-native startups emerged to pioneer LLM-based functionality. From this set emerged scaled startups that have attracted customer as well as investor interest (e.g., Jasper in Copywriting, Warp in Coding). In the AI Legal tools space, new-age startups haven’t emerged in earnest yet (Harvey is the exception); the drive to LLM-based functionality has come from established startups in the market. Some key factors driving this are -

Lack of a lower-end market - Across both Copywriting and Coding markets, new startups had a large set of individuals / small businesses to sell to (Freelancers, developers, marketers, etc.). Traction and product evolution in these segments allowed successful startups to then move up towards Mid-market and Enterprise. In the Legal space, the uses cases for individuals are scarce to non-existent. And law practices, including solo practitioners and small shops are well served by Legal Tech incumbents.

High bar for accuracy - Requirement for accuracy is higher in Legal than other markets, given the precise nature of legal process and potentially large consequences for small mistakes. The recent case of 2 lawyers being sanctioned for citing fake cases emerging from ChatGPT highlights the risk. Players with access to legal / customer data for training have a significant advantage - benefiting existing players.

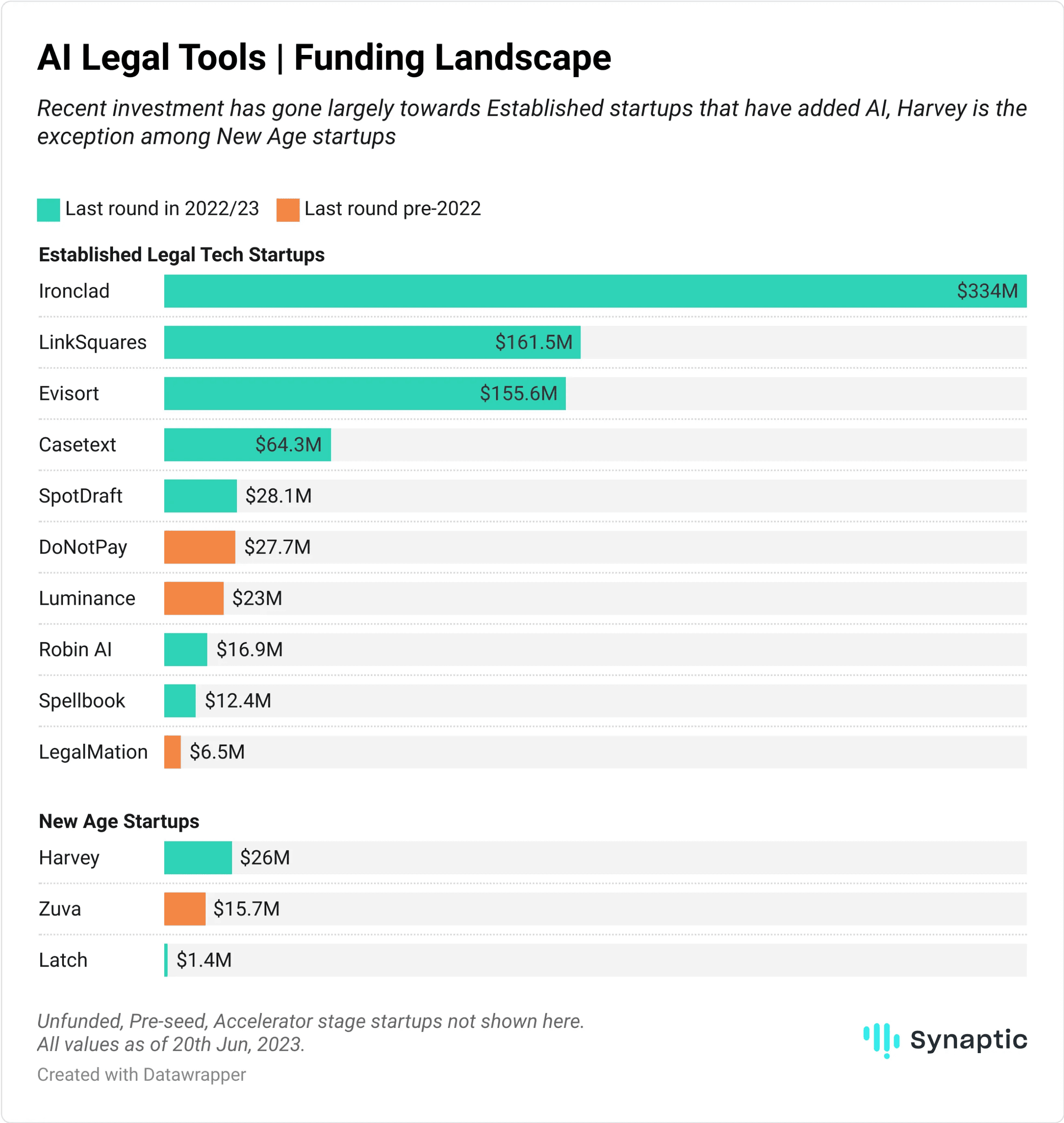

Funding Landscape: Recent investment activity has largely targeted Establised Legal Tech Startups

Incumbents / established startups are better positioned to deploy LLM use cases than New startups given access to distribution and data. It is therefore not surprising that funding dollars have been directed towards relatively established players in the space.

Ironclad, LinkSquares, Evisort, Casetext, SpotDraft have all raised recent rounds with AI-based features a stated objective in the raise.

Harvey is an exception among new-age startups. An OpenAI-funded startup, it hit the headlines for it’s deal with Allen & Overy and has subsequently raised a $21M series A (Apr’23) led by Sequoia. Harvey’s approach has been unique - building bespoke AI models for their customers as collaborative projects vs taking a product-first approach. This has helped them get access and puts them in a great position to attain higher accuracy / relevancy in their offering, which in the future could lead to a killer product which can be transitioned to a product-first model. Perhaps their long waitlist can be an opportunity for other startups looking to capitalize.

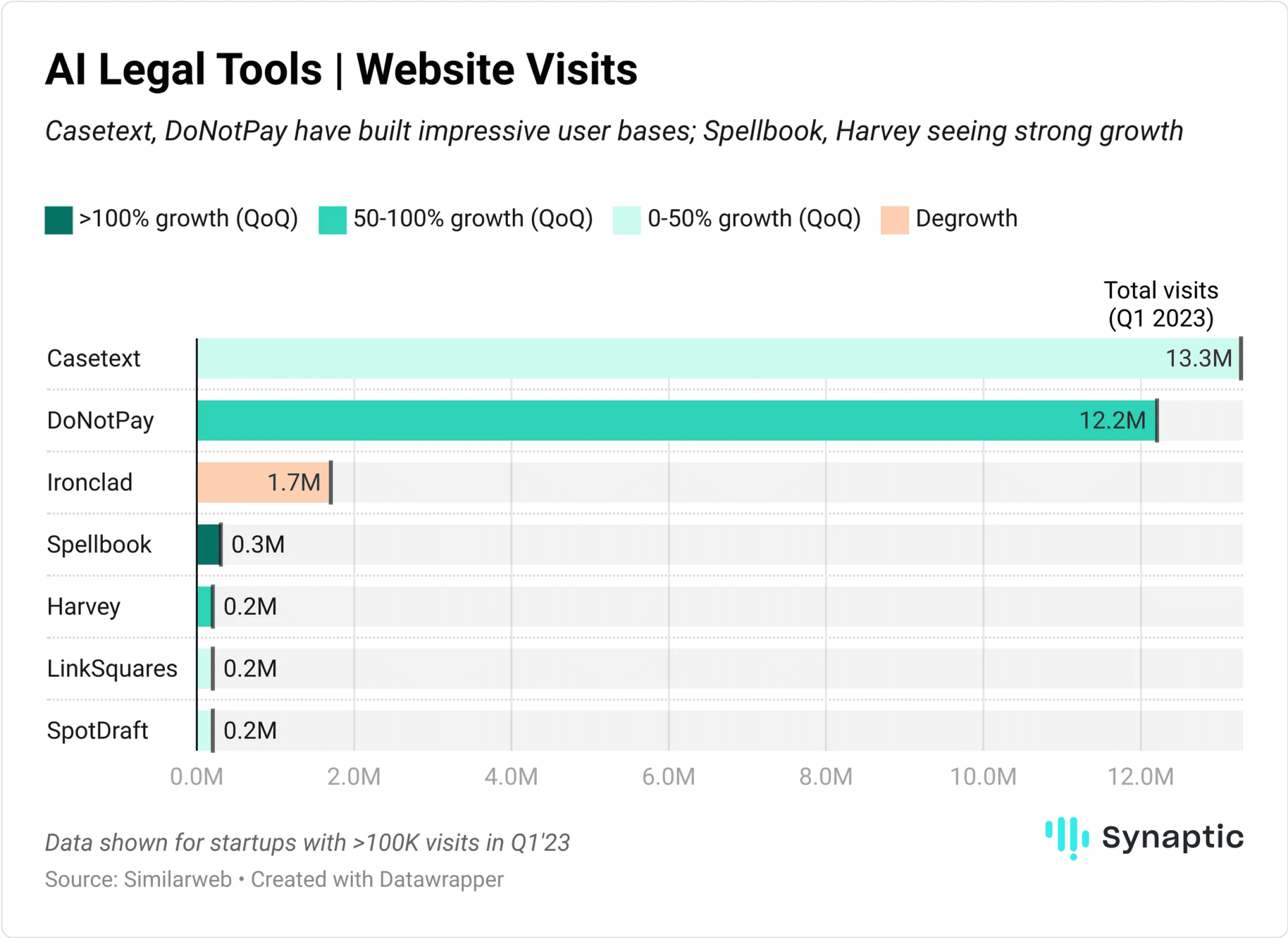

Website traction: Casetext, DoNotPay have built large user bases; Spellbook seeing strong growth

While website visits are not a straightforward indicator of performance in this space as many tools are not just web-based but have integrated applications (like MS Word plugins for contract drafting), there are some clear insights in this data. Casetext and DoNotPay have a substantial and growing user base (10M+ visits is a strong indicator of a big user base) and Spellbook is witnessing superb growth (2.5x visits growth QoQ).

Casetext was an early adopter of GPT3 and was able to get traction in space that has stalwarts like WestLaw (Thomson Reuters) and Lexis Nexis. Recently it has launched Co-counsel a legal assistant. During the publishing of this article, news of Thomson Reuters acquiring Casetext has broken. This makes sense - helps Thomson Reuters keep control of the Legal research space and provides them with a strong LLM-based legal assistant, which they can scale off of their large customer base.

DoNotPay is a pioneer in B2C legal tools, a true market creator. It provides automated legal assistance for small disputes (e.g. rebates, lease disputes, parking ticket appeals etc.) that were often dropped by consumers - resulting in direct savings with very little hassle. LLM-based automated bots have taken the product to another level.

Spellbook is contract management player targeting lawyers and legal practices (which is rare as most contract mgmt. solutions target corporate) with LLM-based automation for complex / bespoke contracts (the kind that would come to lawyers rather than being handled by corporate legal). The native MS word integration and innovative features like negotiation suggestions and auto-diligence set the tool apart. It’s strategic partnership with Thomson Reuters is another differentiator that allows access to customers and data.

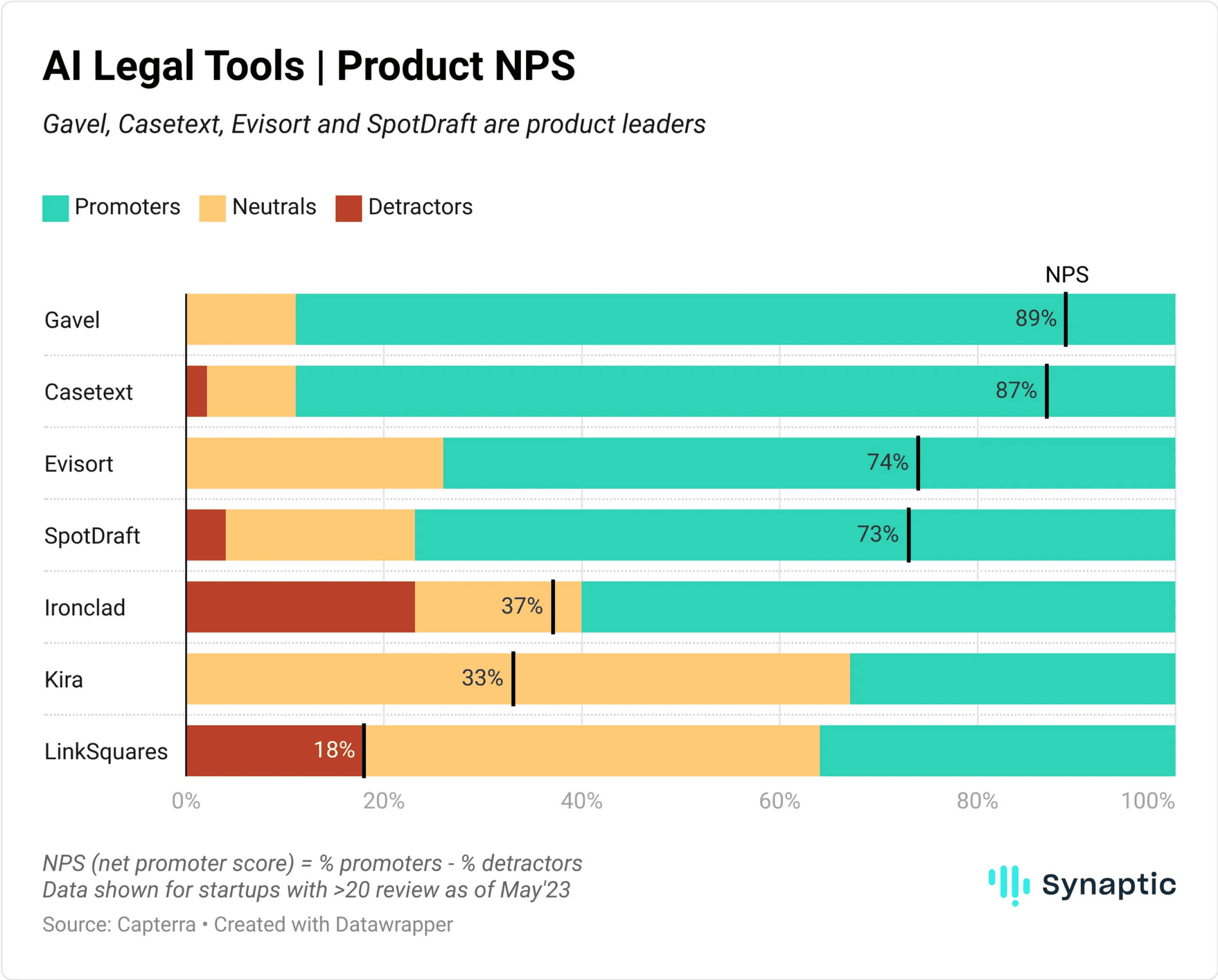

Product Feedback: Gavel, Casetext, Evisort and SpotDraft are product leaders

Casetext’s product feedback underscores its strong traction and gives credence to Thomson Reuters’ rationale for acquiring it. Evisort is a well-established player and product leader in the contract management space.

Gavel (formerly Documate) is an emerging player in the legal documentation space with a unique approach - Gavel enables legal practices to create client facing workflows that help them deploy legal products along with their services (e.g. Gavel helped a small legal practice launch a rental lease agreement tool for its customers). The strong automation features, workflow integrations, and prompt customer support are key drivers of NPS.

SpotDraft is an emerging player in contract management. The product differentiation is based primarily on superior workflows (large set of integrations, central contract mgmt feature that tracks all changes, tasks related to contracts) and ease of setup.

Looking Forward

Killer LLM-based products are yet to emerge

While multiple startups have built LLM-based functionality, there isn’t proof of transformative value addition yet (similar to say the significant productivity benefits of AI Coding Tools). Who cracks the first killer LLM product is the most important question of 2023. Harvey, DoNotPay and Casetext would be our bets.

Growth-equity investor’s market

The most interesting startups in the space - Harvey, DoNotPay, Spellbook, SpotDraft have all raised at series A / B, and will be opportunities for series B / C investments in the near future. Casetext’s acquisition also illustrates potential for M&A; deals and buyouts in the space as startups scale.

Market will evolve through partnerships/acquisitions

Partnerships and M&A will be an important aspect of how the space develops. Thomson Reuters for example has pledged to invest $100 million in exploring generative AI for Legal. This has resulted in launch of new Westlaw Precision product, an investment in Spellbook, a partnership with Microsoft to integrate with 365 Copilot and now a $650M acquisition (admittedly more than the $100M they publicly committed) of Casetext. Other incumbents will undoubtedly be looking for M&A; opportunities as well.

AI Legal Tools is a market on the precipice, with clear potential for value but big challenges to achieve practical accuracy; we wait to see who can “raise the bar” and unlock this opportunity.